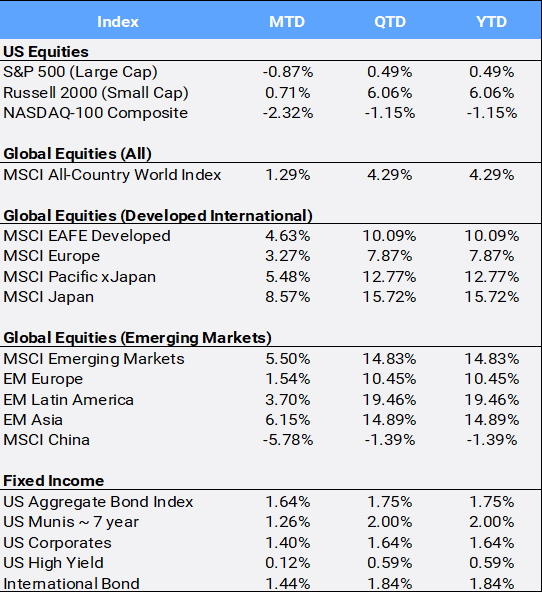

Global stocks marched 1.29% higher in February to bring YTD returns to 4.29%, following 2025’s 22.34% gain. The MSCI All Country World Index’s (ACWI) made four new all-time highs this month. February was a challenging month for US large cap stocks as the S&P 500 fell 0.87% MTD amid growing scrutiny of AI-related capital expenditures and their associated impact on business models. A higher‑than‑expected producer‑price reading released on the final trading day revived inflation worries and dampened expectations for Fed rate cuts. However, February may have been less of a selloff, and more of a rotation, as the SPW equal-weight index gained 3.40% MTD to bring its YTD return to 6.78% compared to 0.49% for the market-cap-weight index.

Source: Bloomberg Pricing Data, as of February 28, 2026

Click image to enlarge

- The CBOE S&P Volatility Index (VIX), often referred to as “the fear index”, climbed to 19.86, up 32.84% from where it started the year at 14.95. Unsettling markets are President Trump’s unclear tariff policies and military tensions between the US and Iran. On Friday’s last day of trading for the month, Trump said that he’d “love not to” attack Iran, “but sometimes you have to.” Then on Saturday the 28th, he did: launching “Operation Epic Fury” with the goals to eliminate Iran’s nuclear programs and to facilitate regime change. Traders are also assessing the geopolitical and economic uncertainty following the February 22 US Supreme Court decision striking down Trump’s emergency tariffs.

- Bonds wrapped up February with “the Agg” posting its best monthly rally in a year, surging 1.64% MTD amid fresh concerns of AI’s disruptive impact, escalating global tensions, and concerns about hidden vulnerabilities in private credit. US Treasury short-term yields fell to levels last seen in 2022, as the two and ten-year rates finished February at 3.37% and 3.94%, respectively. In addition, the average rate on the 30-year fixed-rate mortgage (blue line) fell below 6% for the first time since September 2022.

- The Producer Price Index rose 0.5% MoM and 2.9% YoY in January as services sector margins surged, suggesting businesses were passing on tariff-related costs along to consumers. Adding to inflation concerns, rare‑earth metal shortages pushed up input prices for aerospace and semiconductor firms. China’s control of the rare earth market is likely to be a key topic between Presidents Trump and Xi when they meet in Beijing next month. For global markets, China was the largest detractor to global returns in February falling 5.78%.

- On the other side of the international markets return coin was Japan who was the largest contributor to ACWI returns (2nd largest index holding at ~5% behind the US outsized ~64% weight), gaining 8.57% MTD. The nomination of two pro-stimulus advocates to the Bank of Japan’s board weakened the yen and propelled the Nikkei 225 stock index to record highs. The move, combined with a tame inflation report, may affect the central bank’s plans for future interest rate hikes.

- Korea and Taiwan were the next largest contributors to global returns, gaining 21.78% and 11.83%, respectively. Korea is the leading country in MSCI YTD, up 56.02% so far in 2026. Samsung Electronics, a key supplier of high-bandwidth memory to Nvidia, had the largest impact on global February returns, gaining 35.39% MTD. However, its decades-old partner, Nvidia fell 7.29% this month despite reporting blowout Q4 results. Market participants attributed the decline in shares on doubts around Nvidia’s deal with OpenAI, weak sentiment over the AI trade and skepticism about whether lofty AI capital expenditures are sustainable.

- Seven of eleven sectors gained in February, let by utilities (10.35%) and energy (9.61%) and materials (8.36%). Financials (-6.03%) and technology (-3.59%) were the MTD laggards. Within the Russell 3000 style indexes, value outperformed growth (+2.41% vs. -3.40%), widening their 2026 YTD divergence (+7.04% vs. -4.65%).

- Gold and silver jumped 7.86% and 10.08%, respectively in February, bringing YTD returns to 22.22% and 30.87% with the surrounding unease over geopolitics and the major US military buildup in the Middle East. Crude oil rose 2.78% MTD and 16.72% YTD, while the diversified Bloomberg Commodity Index came in at 1.10% and 11.58% respectively. Fears of another “crypto winter” added to investor anxiety as Bitcoin briefly fell below $60,000 before finishing February down 22.14% and 25.24% YTD.

-

Disclosure Statement

Perigon Wealth Management, LLC (‘Perigon’) is an independent investment adviser registered under the Investment Advisers Act of 1940. More information about the firm can be found in its Form ADV Part 2, which is available upon request by calling 415-430-4140 or by emailing compliance@perigonwealth.com

Performance

Past performance is not an indicator of future results. Additionally, because we do not render legal or tax advice, this report should not be regarded as such. The value of your investments and the income derived from them can go down as well as up. This does not constitute an offer to buy or sell and cannot be relied on as a representation that any transaction necessarily could have been or can be affected at the stated price.

The material contained in this document is for information purposes only. Perigon does not warrant the accuracy of the information provided herein for any particular purpose.

Additional Information regarding our investment strategies, and the underlying calculations of our composites is available upon request.

Data Source: Bloomberg Pricing Data, as of February 28, 2026.

Annual Form ADV

Every client may request a copy of our most current Form ADV Part II. This document serves as our “brochure” to our clients and contains information and disclosures as required by law.

Perigon Wealth Management, LLC is a registered investment advisor. Information in this message is for the intended recipient[s] only. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy will be profitable. Please click here for important disclosures or visit our website at perigonwealth.com.