Steady Through the Storm

War, Uncertainty, Ceasefire and Blockades

The first quarter of 2026 was not an easy one to live through. War broke out in the Middle East. Iran closed the Strait of Hormuz. Oil prices surged. Amidst all this geopolitical upheaval we also saw private credit funds begin gating their funds and limiting withdrawals.

Given everything that has happened, a diversified portfolio has held up well through the turmoil. While broader questions and uncertainties remain; it is worth acknowledging the resilience of portfolios before we get into the details.

What the quarter looked like

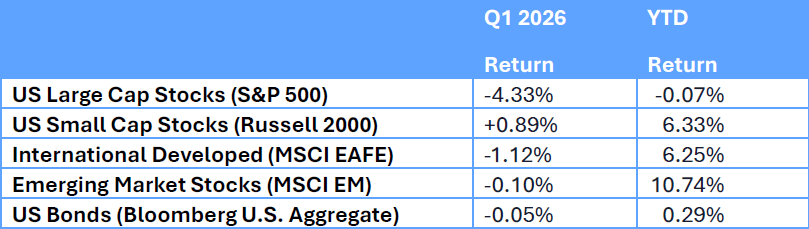

The S&P 500 fell over 4% — its worst quarter since 2022.[1] That is a real decline, and I am not going to minimize it. But the headline number tells an incomplete story. Smaller companies and value-oriented stocks finished the quarter in positive territory, which meant that diversified portfolios experienced a meaningfully different quarter than the S&P 500 alone would suggest.

Source: Y-charts. Q1 returns as of March 31, 2026; YTD returns through April 10, 2026.

Bonds also experienced slightly negative returns but still provided a cushion relative to stocks.

The Strait of Hormuz: oil as the primary transmission channel

Other reasons why the market impact has been contained

First, global oil inventories were near five-year highs before the conflict began, and major economies began releasing strategic reserves early, which gave markets time to adjust without an immediate shortage in developed market economies.

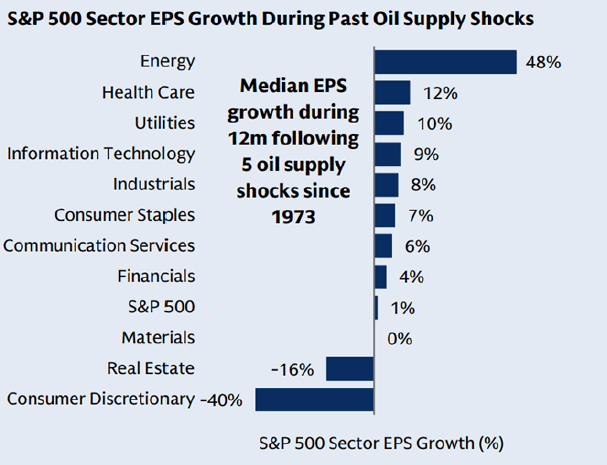

Second, the earnings story for U.S. companies — particularly those tied to the AI investment cycle — remained compelling throughout. Disruptions in the Middle East did not change the fundamental case for technology infrastructure spending, and that underlying strength has provided an anchor for U.S. equities.

Looking at data compiled by Goldman Sachs on earnings per share growth for U.S. companies shows that most sectors have been resilient through past oil supply shocks:

S&P 500 Sector EPS Growth During Past Oil Supply Shocks

A fragile ceasefire, then blockade — what to make of it

I am writing this letter in early April, and while global equity markets rallied following news of a two-week ceasefire; talks broke down over the weekend, and the U.S. has since announced a blockade of the Strait of Hormuz. The outcome ahead is uncertain and even if this is the beginning of the end of the conflict, the path forward is not simply a return to where we started.

Energy prices may ease but are unlikely to fall all the way back to pre-conflict levels. The damage sustained to energy and fertilizer infrastructure is likely to take time to recover from but may also open up investment opportunities going forward. The environment calls for steady, disciplined investing rather than a bold repositioning in either direction.

A note on private credit

One story that has been somewhat overshadowed by the war in Iran but still garnered a fair amount of attention is private credit. Several large funds began limiting client withdrawals after redemption requests outpaced their quarterly distribution limits. The initial cause of distress was concerns about private credit loans made to software companies whose business models are being disrupted by AI. It is worth noting that we continue to monitor the situation closely and have not seen a material deterioration in the overall financial health of the underlying portfolio companies that make up many of these large private credit funds.

However, as investors became concerned about the potential for distress and tried to redeem positions – the issue became pronounced due to the structural mismatch between investors who want to be able to access their money and the underlying assets that are, by design, illiquid.

This is a useful reminder that the attractive yields and returns private credit and other private investment strategies offer do come with a real trade-off between capturing these premiums and liquidity— and that trade-off becomes most visible precisely when markets are already under stress. We could continue to see redemption requests outpace the quarterly withdrawal limits until funds are able to reassure investors of the underlying health of the portfolios and valuation marks. We are monitoring this carefully for clients with exposure to these strategies and remain cautious about allocating additional capital.

[1] Source: Y-Charts Data

[2] Source: International Energy Agency