Global Market Commentary at a Glance

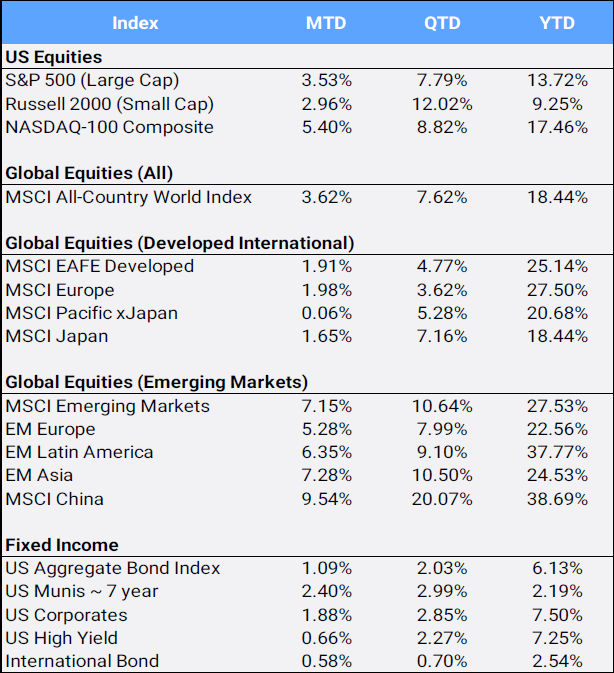

Global equities: +3.62% in September | +7.62% QTD | +18.44% YTD

Dow Jones: Record high at 46,397.89

VIX: 16.28, up 5.99% for the month

Fed: Cut rates by 25 bps on September 17

Gold: +16.83% QTD | +47.04% YTD | $3,886.54/oz. — new all-time high

Bitcoin: +6.54% QTD | +22.33% YTD

S. dollar: Down 7.35% YTD against a global basket

Source: Bloomberg Pricing Data, as of September 30, 2025

Click image to enlarge

Monetary Policy Watch: Rate Cuts and Valuation Warnings

The Federal Reserve reduced its benchmark rate by 25 basis points, marking a continued pivot toward easing. Futures markets now fully expect another rate cut in October and an 88% chance of one more in December.

In an unusual move, Fed Chair Jerome Powell warned that asset valuations are “quite high” by several historical measures — a comment reminiscent of Alan Greenspan’s 1996 “Irrational Exuberance” speech.

The U.S. Aggregate Bond Index gained 2.03% for the quarter and 6.13% YTD, its strongest start since 2020. Treasury yields eased slightly, with the 10-year finishing the quarter at 4.15%.

Market Momentum: September Breaks the Historical Mold

September, historically the weakest month for equities, flipped the script.

The MSCI All Country World Index (ACWI) rose 3.62%, logging 11 new all-time highs for the month and 47 year-to-date.

In the U.S., the Dow Jones Industrial Average hit a record 46,397.89, as investors largely shrugged off fears of a government shutdown.

The CBOE Volatility Index (VIX) rose modestly to 16.28, but remains well below long-term averages.

Advisor takeaway: Timing markets rarely pays off. Even in months known for weakness, strong earnings and rate cut optimism can override seasonal.

Safe Havens and Alternatives: Gold, Silver, and Digital Assets Shine

Gold surged 16.83% in Q3, bringing its YTD gain to 47.04% and setting a new record at $3,886.54/oz.

Silver followed, up 17.44% QTD and 61.39% YTD.

Non-yielding metals often perform well in lower-rate environments. This rally also coincided with uncertainty around a possible government shutdown, which could have delayed key economic data releases.

Bitcoin, often viewed as “digital gold,” rose 6.54% QTD and 22.33% YTD.

Advisor takeaway: When policy uncertainty runs high, precious metals and digital assets highlight the value of non-correlated investments.

Sector and Equity Trends: Small Caps and Tech Take the Lead

Market breadth improved notably in Q3. The Russell 2000 small-cap index advanced 12.02% QTD, signaling broader participation beyond mega-cap names.

Ten of eleven S&P 500 sectors gained, led by:

- Technology (+11.51%)

- Consumer Discretionary (+10.46%)

- Communications (+9.35%)

- Utilities (+7.57%)

Nvidia (+18.10%) and Apple (+24.25%) were the largest global contributors, buoyed by Nvidia’s $100 billion data-center investment with OpenAI.

The only laggard: Consumer Staples (–2.27%), as Kenvue shares dropped following government scrutiny of Tylenol’s potential autism risks during pregnancy.

Advisor takeaway: A constructive sign for long-term investors as the broadening rally beyond large-cap tech points to healthier market participation.

Global Outlook: Emerging Markets Regain Momentum

Emerging market technology companies were among the top global performers this quarter.

- Taiwan Semiconductor: +19.62%

- Alibaba: +17.58%

- Tencent: +16.16%

The China Internet Index climbed 22.37% QTD, and MSCI China (+20.07%) led emerging-market returns, followed by Taiwan (+18.03%) and South Korea (+12.46%). India (-7.61%) was the largest detractor.

In developed markets, Japan (+8.22%), Canada (+11.36%), and the U.K. (+5.07%) were standouts, while Denmark (-13.46%) and Germany (-1.12%) lagged.

A weaker U.S. dollar continued to provide a tailwind for international returns. A diversified basket of non-U.S. currencies gained 7.35% YTD against the greenback.

Advisor takeaway: A softening dollar and renewed tech strength in Asia reinforce the case for global diversification, especially as U.S. valuations climb.

Closing Perspective

September reminded investors that markets often move counter to expectations. Even in a month known for weakness, equities rallied, small caps revived, and gold hit record highs. For long-term investors, the lesson is consistent:

Staying invested, diversified, and disciplined through uncertainty remains one of the most effective strategies for building lasting wealth.

If you’d like help translating today’s markets into your financial plan, we’re here to help.

Disclosure Statement

Perigon Wealth Management, LLC (“Perigon”) is an independent investment adviser registered under the Investment Advisers Act of 1940. More information about the firm is available in its Form ADV Part 2 by calling 415-430-4140 or emailing [email protected].

Past performance is not an indicator of future results. This report does not constitute legal, tax, or investment advice. Investment values may fluctuate and can lose value. The information provided is for informational purposes only and is not a recommendation to buy or sell any security.

Data Source: Bloomberg Pricing Data, as of September 30, 2025.

Annual Form ADV: Clients may request a copy of Perigon’s most current Form ADV Part II. Different types of investments involve varying degrees of risk, and future performance cannot be guaranteed. Visit perigonwealth.com for important disclosures.