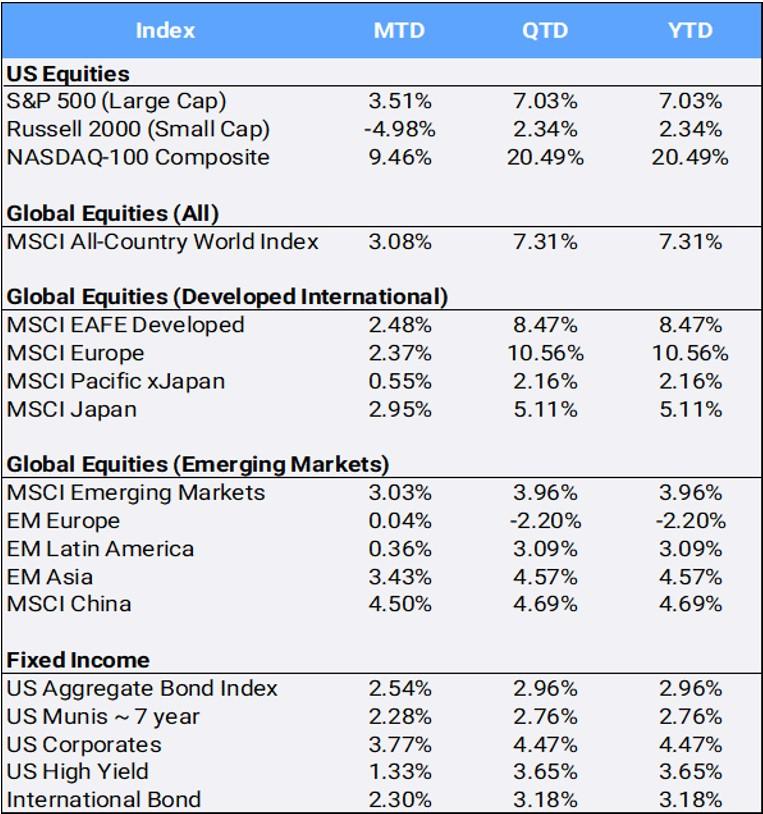

Global equities rose 3.08% in March and were up 7.31% for the quarter, despite much volatility sparked by the abrupt collapse in early March of Silicon Valley Bank and Signature Bank – respectively the second and third largest bank failures in US history—and subsequent weakness in the financial sector. The CBOE Volatility Index (VIX), the so-called fear index that measures volatility (rising when the market is falling), spiked as high as 30.81 intraday on March 13th, before easing to 18.70; it closed the quarter down 13.71% as concerns about the banking sector and inflation numbers moderated and global stocks rallied.

Click the image to view the chart larger.

Source: Bloomberg Pricing Data, as of March 31, 2023

Despite the turbulence, the Nasdaq 100 added 9.46% in March, boosting its quarterly return to +20.49%– its 9th strongest quarter on record for the tech-heavy index since its inception in 1985. By sectors, Technology –last year’s laggard—was the best performing sector for the month (up 10.86%) and the quarter (up 21.65%). Conversely, Financials were in last place, down -9.55% for the month, and -5.55% for the quarter. Energy, last year’s star sector (+64.56%), is in second to last place this year, tied with Healthcare at -4.3% for the quarter. Oil touched a 15-month low in March and is off -5.72% for the quarter.

Large cap stocks, measured by the S&P 500 index, climbed 3.51% in March, outperforming their small cap counterparts as the Russell 2000 index fell -4.98%. For the quarter, large stocks are up 7.03%, whereas small caps only managed to gain 2.34%. Part of that may be due to the small cap index comprising approximately 14 % technology stocks and 16% financials, compared to the S&P 500 ‘s 26% and 13% respective weighting for those sectors. In addition, the S&P 500 financials include institutions deemed “too-big-to-fail”, whereas the small cap banks are regional –weakened after Silicon Valley Bank and Signature Bank’s failures. A further dissection of smaller industries within the Financials sector shows that the KBW Nasdaq Bank Index was the worst-performing out of the entire lineup of Nasdaq-computed indexes, falling -25.2% in March and -18.7% in the first quarter.

Within Emerging Markets, the European countries fell 2.20% in Q1as the only global region that is down so far in 2023. However, European developed markets dominated Q1 regional returns, gaining 10.56% QTD despite a few volatile weeks of trade in the banking sector. Eurozone headline inflation slowed to 6.9% in March, down from 8.5% in February — the sharpest fall on record. European Central Bank policymakers suggested more interest rate hikes are necessary but may come at a slower pace. Despite the shakeup in the banking world, the ECB hiked rates 50 basis points in March. After being the largest detractor from EM returns in 2022 (falling 23.60%), China was able to reverse its fortune so far in 2023, by becoming the biggest contributor to EM returns by gaining 4.69% in Q1.

The collapse of Silicon Valley Bank and ensuing banking crisis spurred chaos in bonds this month. The yield on 2-year notes in early March soared past 5% for the first time since 2007, before reversing to the biggest three-day decline since 1987. U.S. Treasury yields tumbled after the Fed raised its benchmark rate 25bps to a target range of 4.75-5% while acknowledging that rate increases may be coming to an end. Still, the yield curve remains inverted as the 2-year rate closed at 4.03%, above the ten-year at 3.47%. Both started 2023 at 4.43% and 3.96% respectively. Because yields and prices move in opposite directions, global bonds staged a rally as yields came down, with the US Aggregate Bond Index climbing 2.96% and international bonds rising 3.18% in the first quarter.

Internationally, after UBS announced on March 20 it had agreed to buy Credit Suisse, banking crisis concerns spread to other European banks. European Central Bank President Christine Lagarde tried to reassure investors, but shares of Deutsche Bank sank as its credit default swaps unexpectedly jumped. The Bank of England raised rates by 25bps after U.K. inflation reversed recent declines, expanding 10.4% YoY in February. Also, Japan’s core consumer inflation slowed in February largely due to government energy subsidies, as high food and necessities costs persisted.

After gaining 16.09% in 2022, the Bloomberg commodity index fell 5.36% in the first quarter. Natural gas plunged -19.33% in March to tally 1st quarter returns down -50.48%, its worst quarter on record. Gold recorded its second straight quarterly gain, up 7.70% in Q1, as investors bet on the US Federal Reserve slowing the pace of interest rate hikes. Cryptocurrency giant Bitcoin posted its third positive month in a row, gaining 22.67% in March to close at $28,395.30 and post its best quarter in two years (up 71.27% QTD) after navigating its first banking meltdown and another regulatory crackdown.

Disclosure Statement

Perigon Wealth Management, LLC (‘Perigon’) is an independent investment adviser registered under the Investment Advisers Act of 1940. More information about the firm can be found in its Form ADV Part 2, which is available upon request by calling 415-430-4140 or by emailing [email protected]

Performance

Past performance is not an indicator of future results. Additionally, because we do not render legal or tax advice, this report should not be regarded as such. The value of your investments and the income derived from them can go down as well as up. This does not constitute an offer to buy or sell and cannot be relied on as a representation that any transaction necessarily could have been or can be affected at the stated price.

The material contained in this document is for information purposes only. Perigon does not warrant the accuracy of the information provided herein for any particular purpose.

Additional Information regarding our investment strategies, and the underlying calculations of our composites is available upon request.

Data Source: Bloomberg Pricing Data, as of March 31, 2023.

Annual Form ADV

Every client may request a copy of our most current Form ADV Part II. This document serves as our “brochure” to our clients and contains information and disclosures as required by law.

Perigon Wealth Management, LLC is a registered investment advisor. Information in this message is for the intended recipient[s] only. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy will be profitable. Please click here for important disclosures.”

{kind=link}